ngpf calculate shopping with interest answer key: Welcome to the ultimate guide to understanding and mastering the nuances of shopping with interest. This comprehensive resource is meticulously crafted to empower you with the knowledge and skills necessary to navigate the financial complexities of modern consumerism.

Within these pages, you will embark on a journey of financial literacy, delving into the intricacies of loan calculations, comparing loan options, and crafting a budget that aligns with your financial goals. We will also explore the responsible use of credit and equip you with the tools to make informed financial decisions.

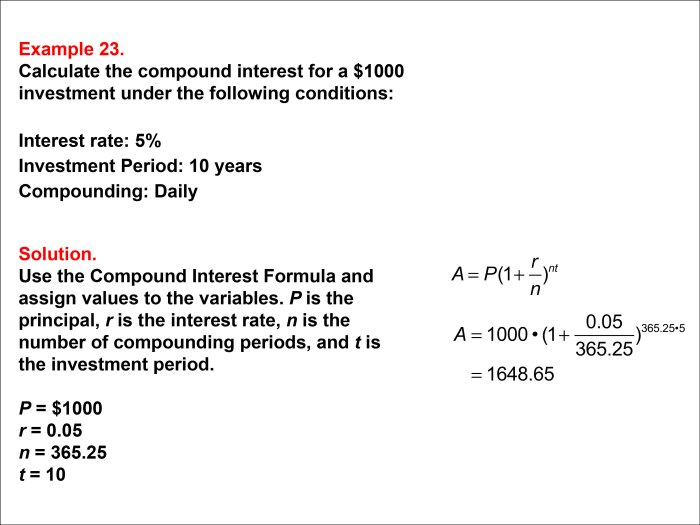

Calculate Interest on a Loan

Calculating interest on a loan is essential for understanding the total cost of borrowing. The formula for calculating interest is:

I = P

- r

- t

Where:

- I is the interest

- P is the principal (the amount borrowed)

- r is the interest rate (as a decimal)

- t is the time (in years)

For example, if you borrow $1,000 at an interest rate of 5% for one year, the interest would be:

I = $1,000

- 0.05

- 1 = $50

The different factors that affect the interest rate on a loan include:

- Your credit score

- The loan amount

- The loan term

- The type of loan

- The current economic conditions

Compare Different Loan Options

There are a variety of loan options available to consumers, each with its own advantages and disadvantages. The most common types of loans include:

- Personal loans

- Auto loans

- Mortgage loans

- Student loans

- Business loans

When comparing loan options, it is important to consider the following factors:

- Interest rates

- Fees

- Terms

- Prepayment penalties

The best loan option for you will depend on your individual needs and circumstances.

Create a Budget for Shopping: Ngpf Calculate Shopping With Interest Answer Key

Creating a budget for shopping is essential for controlling your spending and avoiding debt. To create a budget, you need to track your income and expenses.

Once you know how much money you have coming in and going out, you can start to allocate your funds. A good rule of thumb is to allocate 50% of your income to needs, 30% to wants, and 20% to savings.

There are a number of different ways to track expenses, including:

- Using a budgeting app

- Creating a spreadsheet

- Using a notebook

The most important thing is to find a system that works for you and stick to it.

Use Credit Wisely

Credit can be a valuable tool, but it is important to use it wisely. When you use credit, you are essentially borrowing money from a lender.

There are a number of benefits to using credit, including:

- Building your credit score

- Making large purchases

- Covering unexpected expenses

However, there are also some risks associated with using credit, including:

- Paying high interest rates

- Getting into debt

- Damaging your credit score

To use credit wisely, it is important to:

- Only borrow what you can afford to repay

- Make your payments on time

- Keep your credit utilization low

Make Informed Financial Decisions

Making informed financial decisions is essential for achieving your financial goals. To make informed financial decisions, you need to:

- Understand your financial situation

- Research your options

- Consider the pros and cons of each option

- Make a decision that is in your best interests

There are a number of resources available to help consumers make informed financial decisions, including:

- Financial advisors

- Credit counselors

- Government agencies

- Nonprofit organizations

By taking the time to make informed financial decisions, you can improve your financial well-being and achieve your financial goals.

FAQ Insights

What is the formula for calculating interest on a loan?

Interest = Principal x Interest Rate x Time

What are the different types of loans available to consumers?

Personal loans, auto loans, mortgages, student loans, and credit cards

What are the advantages of creating a budget?

Helps track expenses, control spending, and achieve financial goals